Investing has multiple schools of thought which have been known to generate high returns at different points of time in the past. Practitioners often hold passionate debates about the superiority of their style vs others. But in my experience, no 1 method is perfect, and the chosen style depends on the individual investor’s risk appetite, corpus size, psychology, knowledge, and experience. Now, I’ll talk about some popular styles of investing:

Value Investing

This style is tailor made for the conservative or cautious investor. I also suggest this to my friends who are starting out. It was popularized by Warren Buffett and today has millions of followers. The idea is to buy companies at a discount to their intrinsic value and sell them when they reach fair valuation or hold them if their future is bright. Valuation will be discussed at length later in this blog. Generally, value investors look to buy cheap stocks trading at a P/E multiple of < 20.

Growth at a Reasonable Price

A relatively new style of aggressive investing which has caught the fancy of the current generation of investors. In this style, growth is treated as a component of value and hence richly valued companies growing fast are eagerly sought. GARP investors don’t mind paying 50-60 times P/E multiples for a company if its profits are growing at a rate of 20%+. Fast growth justifies paying a high price upfront. This is riskier than value investing because GARP investors assume that companies will either match historical growth rates or surpass it. Not all of them do and hence some GARP investors do end up losing money. The upside is that if they are correct, then they end up making a lot of money because often the market underestimates the valuation and potential of high quality GARP stocks.

Consistent Compounders or Buy at any price (BAAP)

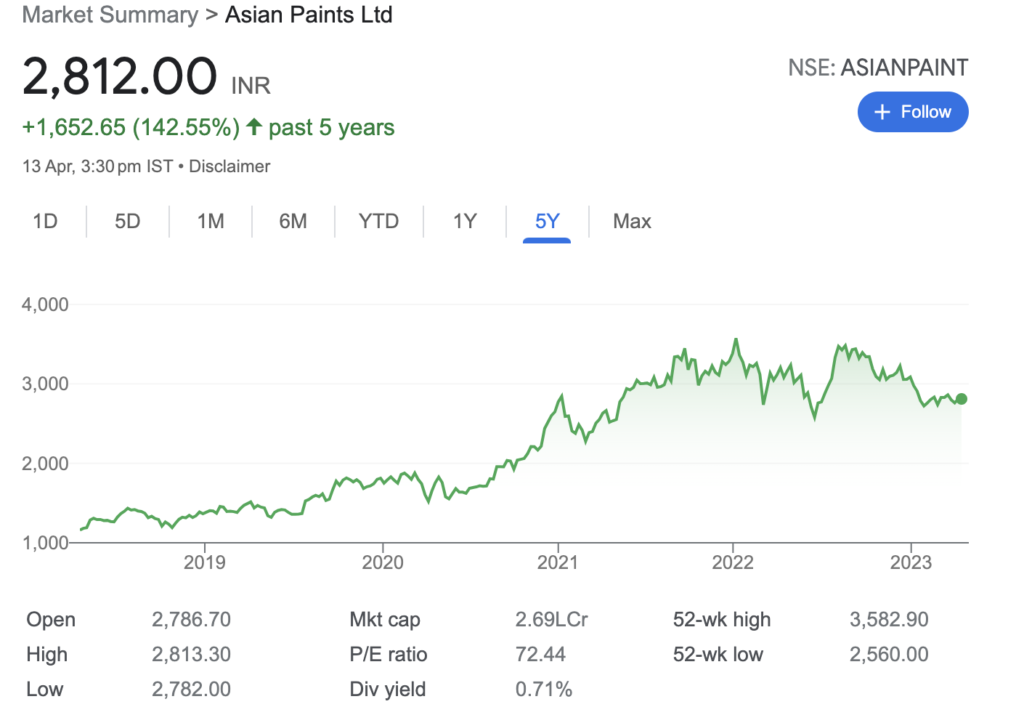

Consistent Compounders is a term popularized by the team at Marcellus. Terry Smith, another famous fund manager, is also an advocate of this approach. The goal is to buy high quality companies irrespective of the valuation which could be anywhere between 80-120 times P/E. High quality here refers to companies being debt free, deploying capital at rates significantly above their cost of capital, and consistently generating huge free cash flows. They run back testing models to show that had an investor even paid 200 times the multiple of a certain stock 10 years ago, he would still have ended up making close to 10x on his investment. This is great in theory where you just buy and forget about your investment. However, reality is a little different, because there are so many factors which impact the returns generated that one can’t simply buy an expensive stock and hold it for a long time.

Instead of an Asian Paints you could end up with a Wipro which took 20 years to break it’s all time high achieved in the dot com boom. One should be very careful and think twice before buying expensive stocks.

Special Situations

This is a relatively less practiced form of investing where the focus is on taking advantage of the market’s poor record in pricing a demerged entity, change of management, delisting, buy backs and acquisitions. This is probably the fastest way to generate alpha if one can correctly time the entry and exit. However, to be able to do so on a consistent basis is very difficult to achieve as sometimes the market does price the special situations very fairly and the investor could end up taking a loss if he has bought the stock in the initial euphoric phase.

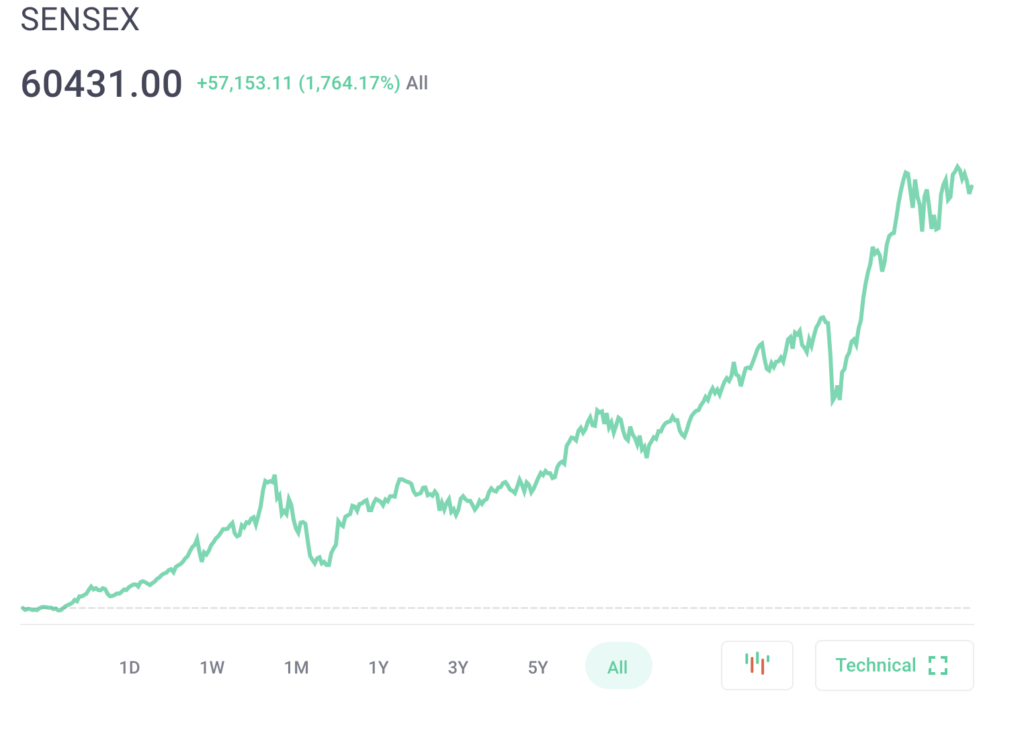

Indexing

There are mainly 2 types of people who invest in Index funds. One is the believer of the efficient market hypothesis which states the stock price reflects all there is to know about its fundamentals and hence there is no point in buying individual stocks to generate alpha, as they can never beat the index. This theory has been proven wrong time and time again by the successful track record of so many fund managers that I won’t talk further about it. The second type of people are those who either don’t have time to study individual stocks or would like to diversify their portfolio. Indexing is still better than investing in bank fixed deposits.

Peter Lynch Method

This method inspired by its namesake suggests that one should invest in stocks of those companies that one sees in its environment, uses himself on a regular basis and has a deep knowledge of. Most B2C companies would be covered under this method as we all use toothpaste, eat cereals, buy clothes, shop online etc. Some B2B companies could also get included as a lot of businessmen use some listed component manufacturers. Go check your car tyre brand. Doctors know which medicines work the most. Their understanding of the pharma industry would also be far better than that of an outsider. Similarly, try applying this style to your life and think which stocks should you own?

Proxy investing

Sometimes when an industry is fragmented or too complex to understand or very cyclical then instead of investing into any of these stocks directly which could be risky, a smarter move is proxy investing which seeks to invest in the same supply chain either upstream or downstream to take advantage of the huge aggregate demand for the entire industry. This way you get exposure to the industry’s boom without the baggage of holding some difficult to understand players or cyclical players.

The point is no style works 100% fine all the time. A lot depends on macro, micro and stock specific actions. It’s not advisable to keep switching your style to suit the flavor of the season. Choose one in which you have maximum conviction and can continue with good and bad times. Your mistakes will be lesser and you will have a higher probability of catching multibaggers.

Leave a Reply