If you are reading my blogs for the first time, I would recommend you start with the blog on Investing Styles. Once that is done, here are certain investing models that have stood the test of time and helped countless investors understand how the market works and prices certain stocks. Some of them are borrowed from other disciplines and can be applied to other areas of life as well. For now, I have described some essential mental models that every investor must know of (and in a later blog I will recommend some more good books that an investor can read to learn more mental models and fine tune his process).

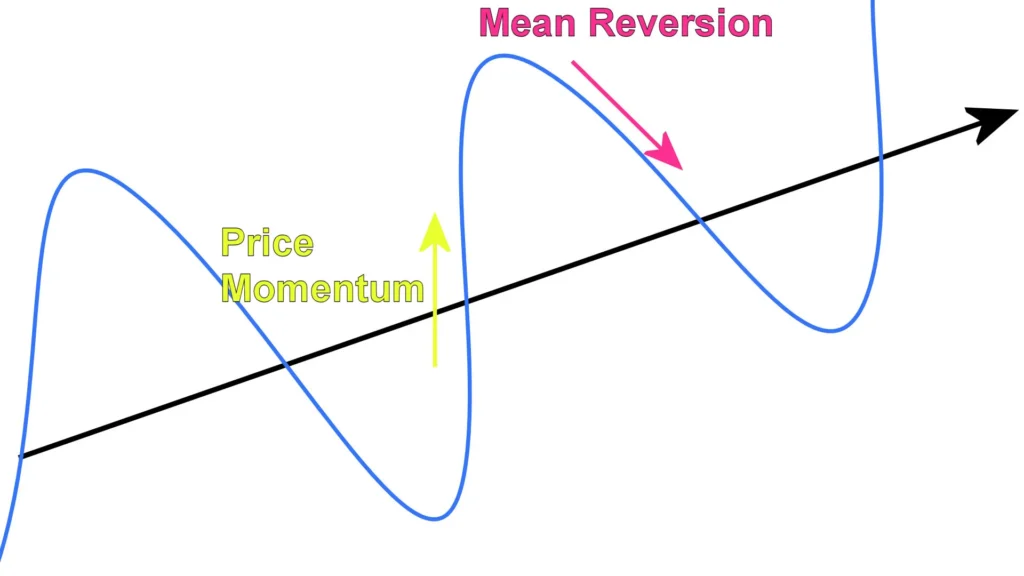

Mean Reversion

This is an important mental model especially when it comes to investing in cyclicals and consistent compounders. You might wonder how one theory can be applied to such an odd combination but hear me out. Cyclicality is about mean reversion when it comes to sales and profits growth rates. The best practice is to buy when they are trading below their average and to sell them when they are trading at a multiple above their average. Even if you’re unlucky and can’t book the top, you’ll still have made a decent profit by selling above the mean multiple. Advocates of consistent compounders must know that with a sustained hike in interest rates or a general economic slowdown there could be a harmful impact on the multiples commanded by consistent compounders. There could be a derating to the historical average PE thereby even if the earnings grow, the returns will be offset by a lower multiple.

Second Order Effects

This refers to the consequences of consequences. Most investors don’t understand or are blind to second order effects which puts them at a huge disadvantage. Capitalism encourages zero sum based games where there are winners and losers. Actions have consequences which have their own consequences. We often fail to map out and fully comprehend this second level of impact and how it can affect our investments. Just like in game theory, we can try to map out the behaviour of several players within an industry and figure out how they are going to respond to each other’s actions (how would the consequences change depending on the decision taken). There can be third or fourth order effects as well but they can be too varied in terms of outcome to calculate, hence we should focus on the immediate impact of consequences of our actions.

Circle of competency

When it comes to investing, stay within your zone of comfort, knowledge and understanding – also called as circle of competency. The further you stray away from this circle, the higher are your chances of incurring a loss due to some unforeseen risks which you weren’t aware of due to knowledge and understanding gaps when it comes to that particular industry or stock. This is not to say that one can’t increase their circle of competency to accommodate more and more industries. But this process is rather slow and can take a while. The investor has to be patient, continue his research and avoid any unnecessary risk

Reflexivity

This was developed by the legendary investor – George Soros. It refers to the phenomenon of rising stock prices leading to higher investor expectations which leads to a surge in buying making prices rise further and so on resulting in what we call a positive feedback loop. However, the reverse can also happen when lower prices lead to reduced investor expectations which leads to more selling causing the prices to go even lower and so on.

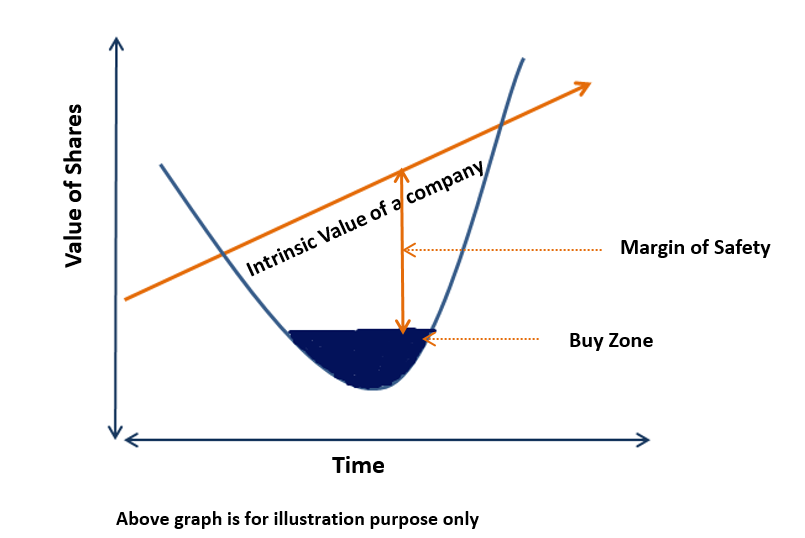

Margin of safety & danger

Every investor should ensure he has a margin of safety when he invests in a stock. Here margin of safety refers to having a room for error either in one’s position sizing or valuation such that if the stock falls, the absolute loss, and relative impact on portfolio level returns is minimized. Similarly, if a client invests in a stock which is very overvalued, then it suffers from a margin of danger means there is absolutely no room for error, and a fall in price could significantly impact the investor.

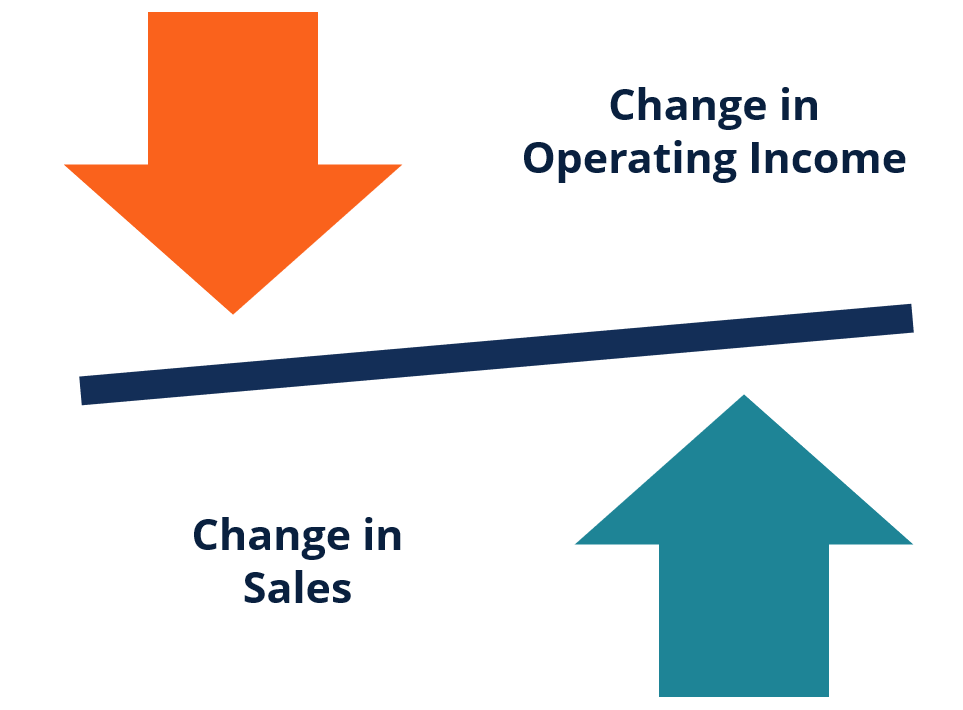

Operating Leverage

A very powerful theory that most investors have difficulty grasping. The higher a company’s fixed costs, the faster will be its profit growth with an increase in sales. This is very important so let’s understand this with an example. Let’s say I run a pharmaceutical company which has 60% fixed costs and 10% variable costs. So, if the sales are Rs. 100, the fixed costs are Rs. 60 and the gross profit is Rs. 30. Now if the sales grow by 10% to Rs. 110, the fixed costs stay the same at Rs. 60, the variable costs also go up by 10% to Rs. 11, the gross profit now is Rs. 39. Thus a 10% increase in sales leads to a 30% increase in profits when fixed costs are so high. The same non-linear relationship exists on the way down as well. Operating leverage results in disproportionate movement in profit due to an increase or decrease in sales.

Inversion

This mental model was popularized by Charlie Munger. Instead of approaching the problem head on and trying to find the best solution, Charlie suggests us to reverse our approach and figure out all potential solutions which will not solve the problem. In this way, we can isolate and find the correct answers. It’s often easier to answer in negative than positive where the list could be much bigger, hence the rule to always invert. In investing, we should not be concerned with finding multibaggers. Multibaggers are the result of a well thought process. Rather our goal should be to minimize or avoid losses. This in turn will automatically generate handsome returns for us.

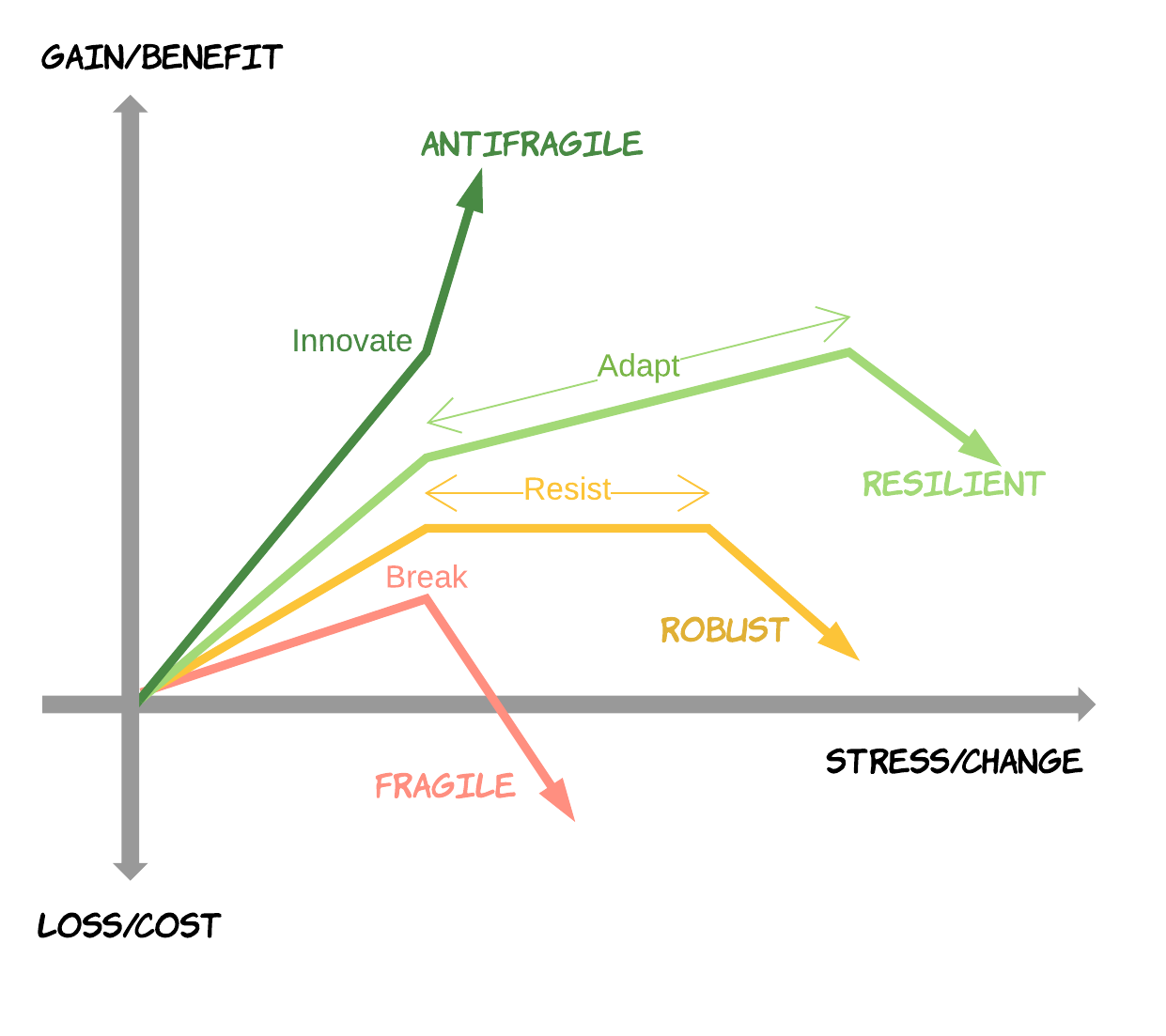

Anti-Fragility

Some companies are resilient to shocks and are able to survive. Some companies become more robust and thrive when faced with shocks. This 2 nd category of companies are called anti-fragile. Shocks can come in any unpredictable form, and we can never assess their impact in advance. However, due to the nature of their work and strong business model, some companies can tackle shocks head on and become stronger in the process. Think of vaccine manufacturers during Covid. They did spectacularly well when the world was suffering. Now forget Covid for a minute, in both good and bad times, the world will continue to need vaccines. If there is any natural or man-made disaster, the local population’s health will be affected and demand for vaccines will increase. Hence irrespective of most types of shocks, vaccine manufacturers will continue to benefit and thrive.

Pre mortem

I learned this model from a book by Michael Mauboussin. Instead of conducting a post- mortem like examination about the likely causes of our stocks falling, we should do a pre- mortem before we buy any stock where we should try to clearly outline various reasons as to how the stock could underperform or even fail. If successfully done, then it can help us avoid duds and build conviction in the stronger names. Then the usual volatility won’t affect us and probability of committing a mistake will reduce.

Probabilistic outcome

Investors should always think in terms of probabilities. The stock market like horse racing functions as a pari-mutuel system. This means we don’t just have to think about the probability of our chosen stock delivering great returns, we also must factor in the odds that the market is offering us to make the bet. If the market considers the stock to be an obvious winner, then the odds offered will be such where the payoff in our favor is very low. We make the most money when the market misprices the bet and offers us odds, where the upside is huge and downside is low.

The 80/20 rule

:max_bytes(150000):strip_icc()/GettyImages-1044950388-a012d288b7724351a9d0a8e72a85e581.jpg)

A fact that will showcase itself over the long term: 20% of our portfolio holdings will generate 80% of our returns and vice versa. This is surprising for most investors who have been bombarded with the advice that one should have a concentrated portfolio and hold as few names as possible – why because a famous investor said so. If you keep this model in mind, you’ll know that having a concentrated portfolio doesn’t make sense unless one is a genius or an expert, because your probability of generating good returns is greatly diminished.

Base Rates

Investors should always be mindful of base rates when analyzing businesses. Base rates refer to the long-term average outcomes/growth rates. They obviously vary by industry and business model. Hence, when an investor comes across a business which is growing significantly faster than the wider industry itself, he should try to find out the reasons behind this positive deviation – is the company gaining market share from competitors, is the company able to increase customer wallet share, is there a possibility of fraud due to unbelievable/overoptimistic numbers etc. The company might be growing at 15% which is a very decent number but if the industry is growing at 25% then one needs to wonder why so?

There are over 100 mental models. I have just covered a few must know models in this article. Those who want to become full time investors must develop the habit of cross disciplinary reading. This will help them acquire other useful mental models which could indirectly help them in their investing journey. Mental models are only useful if you apply them in your realday to day life, just reading or memorizing won’t make a difference.

Leave a Reply