Most investors lack a coherent portfolio construction strategy. Making money off individual stocks is easier than making money off a portfolio because not all your stocks will perform well at the same time. Some might even underperform for a period so without a coherent strategy, you might end up selling early or late. Additionally, if you’re too concentrated or diversified, your portfolio will deliver suboptimal returns.

The factors that you need to keep in mind while building your investing portfolio:

Investing style

A lot of people chase fads and latest trends of the day to make higher returns instead of sticking to their chosen style – value investing, GARP, proxy, consistent compounders etc. Even if you plan to mix & match, there needs to be a defined way on how it is to be done. Amateur investors randomly assign a % of their funds to stocks without thinking of the wider impact on their portfolio. Additionally, in crisis times, if some stocks are not aligned with their own investing style, then these stocks are the first to get sold. Always construct a portfolio which represents your individual style and not that of some expert or a friend.

Theme & Industry mix

As India develops, most industries will grow but there will be some industries which will grow much faster than others so it’s useful to have a combination of them in your portfolio. Since we can never know for sure, which industry will deliver the maximum returns or which industry might get sacrificed due to uncertain and unpredictable global headwinds, it makes sense to be exposed to a minimum of 5 and a maximum of 10 unrelated themes. There might be several industries within a theme. Our goal should be to invest in leaders and emerging champions in unrelated themes. If you go for more, your knowledge will be limited and shallow. Best to develop depth of knowledge in your chosen industry and become an expert.

Concentration

If you listen to Warren Buffet and Charlie Munger, they’ll say that you don’t need more than 4-5 stocks in your portfolio. However, most investors don’t have the same IQ and EQ as these geniuses, so we must be more practical in our approach. Research suggests that the ideal number of stocks in a portfolio should be between 15-20 and a maximum of 25. Beyond this your returns will reflect those of the market, and you won’t be able to beat it.

Risk appetite

Are you conservative or aggressive in your approach? Your risk appetite should decide if your portfolio is a mix or dominated by small caps, mid-caps and/or large cap stocks. Small cap stocks are the most volatile and are known to fall 40-60% in bear markets. So, tread with caution and only invest if it matches your approach. Your allocation should be dictated by your risk appetite and not vice versa.

Antifragility

Nassim Taleb developed the idea of Antifragility. We can apply this to the stock market by investing in those companies who either become stronger due to shocks or have the right to conquer different markets and become stronger in the process. There are quite a few industries which are dominated by a few colossal giants while some are complete winner take all situations. When we invest in oligopolistic industries and leaders in consolidating industries, our portfolio becomes stronger in the process.

Knowledge base

This might sound obvious but never invest in companies which you don’t understand because most of you will sell out at the first signs of volatility and not be able to hold such stocks for the long term. You might have a genuine desire to educate yourself on different themes and their respective industries. Then my suggestion is to start small and enter the chosen stock which you don’t fully understand with a small allocation and over time as your understanding deepens, you can increase your position size.

Liquidity

Cash is king and it gives you the power to buy into the market during times of crisis. Usually, I discourage averaging down, but a smart investor can differentiate between a falling knife and a random sentimental fall or fall to due to broader market pessimism which has no bearing on the fundamentals of a good stock. So, if you’re a long-term investor, then keeping a little bit of cash aside in your portfolio can help you take advantage when others are selling in panic. Then you can buy into the fear and get tremendous returns when optimism returns.

The above were some points to keep in mind while constructing a portfolio. You might have noticed that there was no quantitative mumbo-jumbo like they teach in CFA course where they say you should build a portfolio of stocks where correlation is low and then they go deep into calculation of it. In simple words, this is bullshit and just one of the popular theories that have stuck around not because they work but because of a lack of alternate options to provide comfort against uncertainty. The variables involved in calculating correlation are explained in the Capital Asset Pricing Model theory which has been proven useless by countless experts (this is also why there are still legions of people who believe in the efficient market hypothesis another theory which has been proven false but that hasn’t affected its popularity) and correlation itself can’t be proven because most stock returns happen at the tails. For those curious, I suggest reading Nassim Taleb’s recent paper titled ‘Pension funds should never rely on correlation’ which talks more about the correlation issue from a pension fund perspective. However, his arguments are also valid for us regular investors.

Position Sizing

Now that we’ve understood the different factors an investor must keep in mind while constructing his portfolio, it’s time to focus on perhaps the most important factor which can almost single handedly determine his long-term returns: Position Sizing. George Soros, a legendary investor, and trader likes to say – it doesn’t matter how many times you lose, what matters is how much you make when you win and how much you lose when you don’t. It is within this context that position sizing can minimize our risks and maximize our gains assuming we make the optimal allocation across different holdings.

Kelly Criterion

This is most famous and used position sizing technique by investing giants like Warren Buffet, Charlie Munger and Mohnish Pabrai. It has stood the test of time as the original theory was developed back in the 50s and has been successfully adoped by investors and gamblers alike to decide how much % to allocate in a single bet. Here is the exact formula:

K% = W – (1-W)/R

K%= fraction of the portfolio to bet

W= Winning probability

R= Win/Loss ratio

The win/loss ratio is the investor’s edge i.e. how much he makes when he wins and how much he loses when he doesn’t. However, as simple as the above formula may sound, investors must be cautious about the following errors:

- The formula will only be as useful as the accuracy of probability you assign. So, if your numbers are wrong, the result could be something totally different.

- Sometime the Kelly formula suggests allocating 15-25% chunks of the portfolio which could be too risky for the conservative investor.

- Since the Kelly Criterion’s intent is to advise the investor to bet big when the odds are in his favor, it fails to consider black swans and other unpredictable situations.

My style

Instead of a formula deciding how much I bet on a single stock, I want the stock to decide it for me (in terms of becoming a big position by virtue of outsized returns). At the same time, I’m also a fan of concentration to achieve superior returns vs the market. In the past, I’ve tried several methods to see what works best for me (and I stress on the me part here. This is just for education purpose. You need to find a position sizing strategy that works to your benefit and not anyone else’s). I’ve mixed and matched % to check outcomes but again back testing cannot guarantee future success. I’m comfortable holding 4 stocks with 10% allocation each, 11 stocks with 5% allocation each and 5% cash. Some of you might agree, some may disagree. The point is to develop your own independent strategy and stick to it for meaningful gains. A lot of investors are comfortable holding 20 positions of 5% each and letting the market decide. So it’s really up to you to decide what you’re comfortable with.

I have established a broad portfolio construction strategy and explained position sizing, time to go to the next step which is selling criteria. Remember, until you sell and book a profit, all the money is notional and not real. Timely selling can help us nail down our profits, reduce our regrets, prevent losses, and make our portfolio stronger in the process. However, to avoid haphazard and unplanned selling, we must be sure of the reasons. This is where having a defined criteria can help you understand if it’s the best time to sell or not and prevent emotional decision making.

Change in long term outlook

There could be various reasons behind a change in the long-term outlook like the company doesn’t plan any fresh capex for the next 3-4 years, has reduced spending in R&D, has not been able to hire skilled manpower, facing a tough time due to aggressive competitors and reduced customer interest etc. If you feel that the company’s 5–10-year outlook has dimmed, then yes you should consider exiting. You can always reenter when you see tangible signs of the company’s performance improving.

Cheaper, better alternate opportunities

Sometimes emerging stocks when discovered shoot through the roof and generate in 2-3 years’ worth of returns in just a few months’ time. This might sound crazy but such instances do happen time to time. If one of your holdings has got very expensive and you believe there is no further scope for further returns at least for the next few years, then it makes sense to book that profit and invest your money into cheaper, better opportunities that can give you better payoffs. Only sell when you’ve found a better opportunity.

Too expensive price

A lot of investors commit the mistake of confusing high PE with high price and low PE with low price whereas it could very well be the opposite in some cases depending on the industry, product life cycle, competitive positioning etc. The best times to buy is when no one is talking about the company or its industry and the best time to sell is when everyone believes that the company and the industry will perform very well. That’s how you make money.

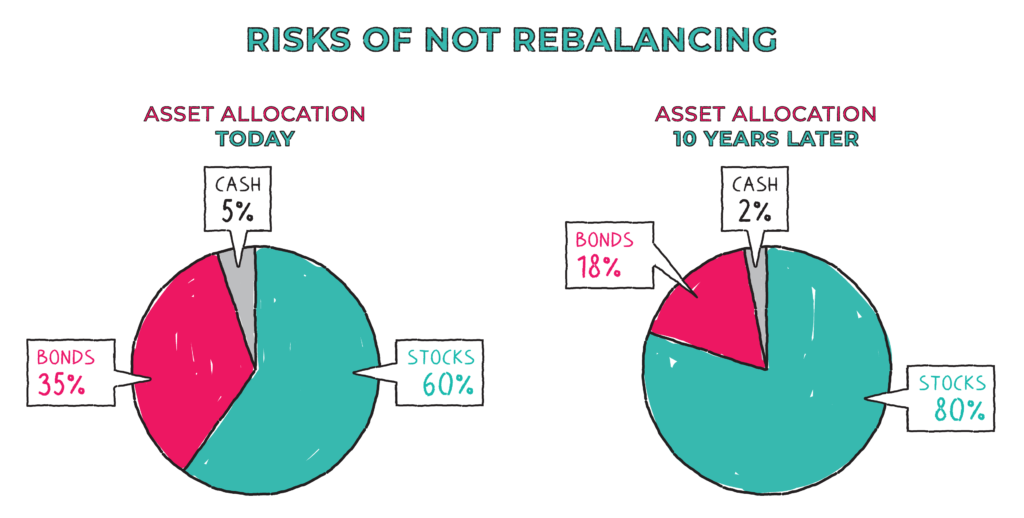

Portfolio rebalancing

When stock returns become more than 20-25% of your total holdings, then it’s the best time to trim your position and rebalance your portfolio by investing the surplus amount into those stocks where your position size is lower or haven’t performed. My general advice is to let your winners run, however we need to act if they become an outsized position. Remember we are concerned with having great portfolio level returns and not just individual returns. Again this might sound obvious and but still is counter intuitive. Hence, portfolio balancing is the way to go as it helps you ride the euphoria as well as buy into the pessimism.

Lack of performance

If some of your holdings have failed to generate insignificant returns or are in loss after 3 years of purchase, then it’s time to get rid of them and make space for new companies. Remember, opportunity cost can be very high so it doesn’t make sense to hold on to companies for longer than 3 years if they have not given us decent returns. You need to analyze your buy decision to figure out what you missed to understand the lack of returns. Later, when the stock starts showing promising signs, you can consider reentry.

Special situations

Yes, an underrated but useful criteria is special situations. If one of your holdings is going for a demerger, delisting, buyback, acquisition etc, then you should take advantage of the market’s mispricing and time your exit as the market goes from complete ignorance to irrational optimism in the way it prices the stock. I repeat this is one of the fastest ways to generate great returns though bear in mind that not every special situation offers great payoffs. One needs to do a proper fundamental analysis of the stock before buying.

There is no perfect portfolio because investors differ in risk appetite, holding periods, circle of competence, goals etc. You need to construct a portfolio which will match your expected level of return while allowing a peaceful night of sleep. If you’re constantly worried and checking stock prices on a daily basis, then your portfolio construction strategy is flawed. Neither extreme concentration nor overdiversification is recommended. The key is finding a balance which will help you achieve your short and long term goals. All you need is 2-3 multibaggers in a portfolio of 15-20 stocks to change your life.

Leave a Reply