Now that we understand the types of moats, it’s time to understand the different types of companies listed in the stock market. If you would like to reread the article on Moats or have not yet read it, I recommend reading that before going ahead. This list has been inspired by Peter Lynch and has some of my own additions.

Fast growers

These companies have consistently grown their sales at 15-20% or more over the last 3-5 years. They need not be small and could be a leader or an emerging challenger in their domain. As India is growing fast and transitioning from a low-income country to a middle-income country, most sectors will do well, and it should be easy to find fast growers in almost every industry. Generally, if the sales grow at 15-20%, the profits will grow at 25-30% which is fantastic for us the investors.

Asset Plays

When a company derives most of its value by virtue of an exclusive or non-exclusive asset that it holds then it is considered as an asset play. These assets could be tangible or intangible. The company could use the asset themselves to manufacture goods or license it out and earn royalty. With each passing year, the value of the asset could keep on increasing or decreasing. Accordingly, the company will act to defend its interests by finding ways to buy more such assets or find ways to improve its lifespan.

Stalwarts

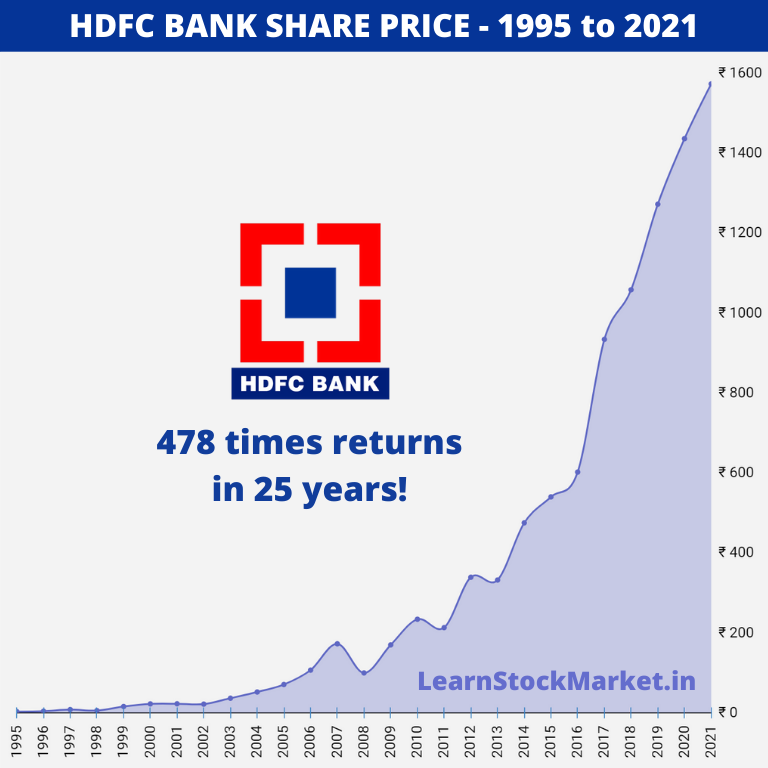

These are fairly mature established companies who grow at about 1.5-2 times GDP growth i.e. 10-15% in India. They are large with widespread distribution of their goods and services. Due to the high base effect, they are unable to grow faster. Stalwart companies are easy to recognize as they are often well-respected industry leaders who after a period of fast growth, have consolidated their operations and now are focused on retaining market share against younger, smaller, and more agile rivals.

Cyclicals

Cyclical companies are those whose profitability depends on the global commodity supply cycle and some degree of government intervention. Buyers have huge bargaining power and often choose the lowest cost producer. Hence, their profits ebb and flow depending on the exact demand-supply situation.

Slow growers

Typically, such companies belong to sunset industries whose heydays are long gone and customer preferences have changed. Their sales growth is < 10%. They continue to produce and deliver till it’s financially viable. Many of them shut shop or get acquired by more efficient rivals. Slow growth is a sign that the future could be bleak unless the company enters a new industry or starts a new product line.

Turnarounds

These are companies transitioning from slow growth to fast growth due to various reasons like new technology, change in management, acquisition, new line of business and sale of loss-making units. The chance to make an Alpha is the highest here because of the rate of change from very negative to highly positive. Those investors who can spot a turnaround opportunity before the rest of the market and ride the whole wave from skepticism to euphoria can end up making astonishing returns in a very short span of time.

Holding Companies

Several such companies exist in the stock market who hold a sizable chunk in another listed player. They don’t run operations as such and their success depends on that of the listed player. They suffer from what is commonly known as the holding company discount since the market knows these companies will never sell their assets and equity to reward shareholders, so the market often devalues their stake in subsidiaries. They key to making money in this is to be aware of price multiple deviation from historical norms and buy it when it is lower than average and sell it when it converges to average historical valuation.

Conglomerates

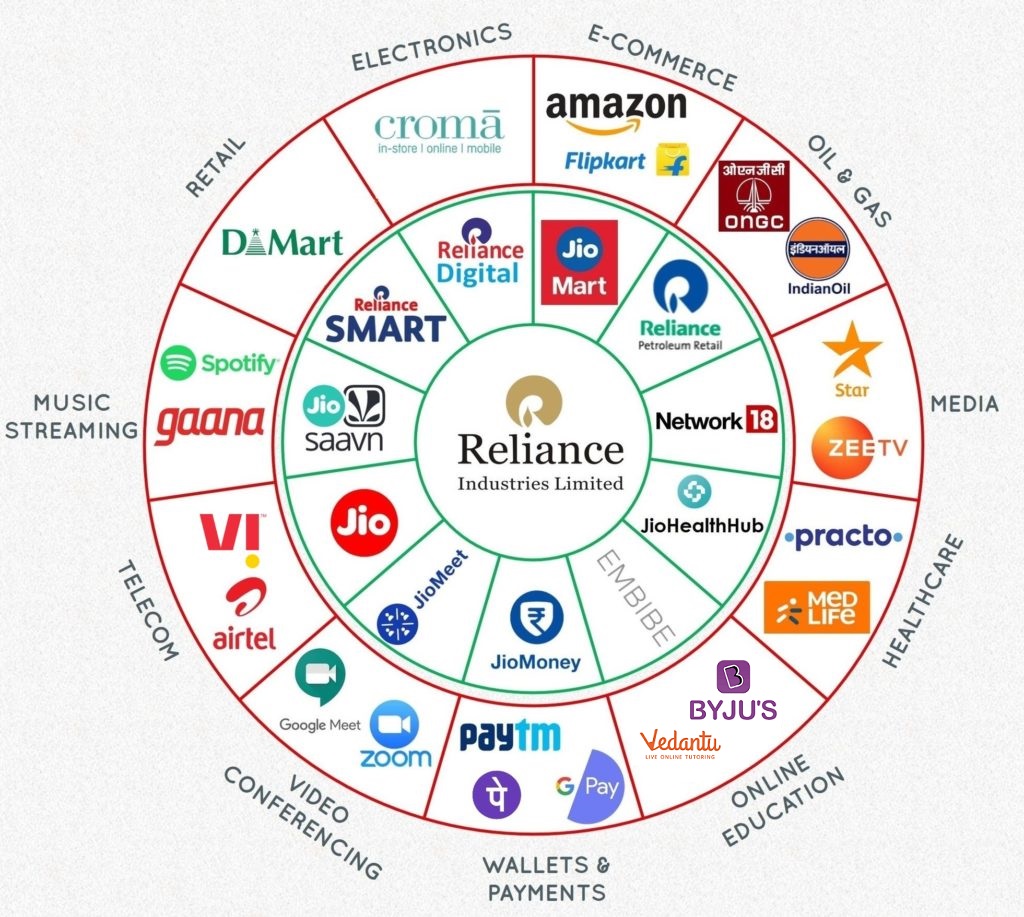

These are mega giant companies who are into multiple verticals. They may or may not be growing fast. Conglomerates are defined by their ubiquitous presence in our everyday lives. They too suffer from what is known as a conglomerate discount which like a holding company discount refers to them being valued at lesser than their parts if listed individually. This is because the market balances the profitable entity against the less profitable one.

One of a kind listed companies

These are players who have no other listed competition. Hence the market rewards them with a scarcity premium which may or may not be justified. This is for the individual investor to analyze. Due to lack of publicly verifiable industry benchmark, they often get lofty irrational valuations which embed all the positives ignore the negatives. Therefore, it’s very important for investors to not buy into the hype and only buy them with a margin of safety.

Bonus:

Banks, NBFCs and other financial companies

The reason why I’m highlighting this is because in my opinion most investors should avoid investing in the financial sector. This is because such companies can easily manipulate their books through multiple ways and dupe investors both big and small and not get caught until it’s too late. In India, there have been so many cases of banking fraud. The recent ones being PNB, Yes Bank, DHFL where investors have lost thousands of crores. The financial sector is poised to boom as India grows so bold investors can allocate a small % of their portfolio and gradually increase the stake as their understanding of all potential inherent risks increases.

Often companies have overlapping characteristics. Additionally, they do not work in isolation and their actions are often subject to reactions by competitors. So, while it’s good to identify and understand the company, a good practice is to map out the entire industry first and at least have a bird’s eye view of it. Ideally, one should do a detailed comparison between different players to know each’s strengths and weaknesses. But this can be challenging to achieve for those short on time or whose knowledge of the industry is still elementary. Rome was not built in a day so you shouldn’t be too harsh on yourself if every aspect of a company’s business or industry is not 100% clear to you. Just like a tea is enjoyed with small sips, you too can start your journey with the company by buying a small position and gradually increase your stake when your understanding increases (leading to more conviction).

Leave a Reply